U.S. Housing Starts: Mid-Year 2026 Update

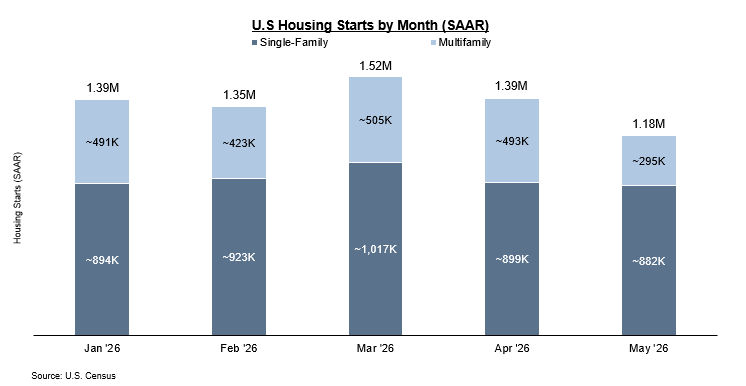

Following a strong March and April, U.S. housing starts declined ~15% month-over-month in May to a seasonally adjusted annual rate (SAAR) of 1.18M. This is the first time the SAAR for housing starts has dipped below 1.2M since the beginning of the pandemic in May 2020. Analysts originally projected May's SAAR to grow to ~1.43M, so its result fell well short of expectations.1

A resilient multifamily market helped prop up a declining single-family market in the first few months of the year, but the multifamily sector took a big hit in May with starts declining ~40% month-over-month to 295K.2

Builders and Buyers Face Affordability Pressures

High home prices, elevated mortgage rates, and increasing building material and labor expenses continue to impact home builders and buyers. The National Association of Home Builders (NAHB) reports that, “Elevated mortgage rates, affordability challenges and cautious buyers continue to weigh on demand for new homes. Builders are offering incentives and cutting prices, but difficult market conditions are still limiting sustained momentum for new construction.” 3

At the beginning of the year home builders were already facing elevated material costs, which became further exacerbated by the Iran war from March onwards. The NAHB reports that, “With oil prices higher in the U.S., 62% of builders reported suppliers have increased building material costs due to higher fuel prices, including gas and diesel.”4 Home builders should see some cost reductions if a peace deal is officially signed between the U.S. and Iran, but even prior to the war material costs were already ~40% higher than 2020 levels, so builders will still have to navigate significant cost pressures.5

As of June 18th, the average U.S. 30-year fixed rate mortgage is 6.47%, down from 6.84% in June 2025, but higher than the 5.98% rate in early 2026.6 Financial markets believe a Fed Reserve rate cut is unlikely in H2 2026 and a rate increase is a possibility.7 With rates remaining at these levels we are unlikely to see drastic changes in the single-family housing market.

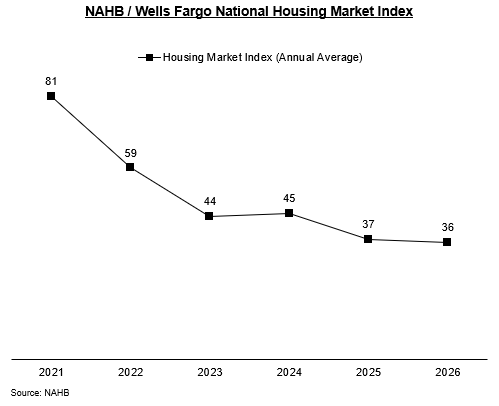

This sentiment is shared by home builders, according to recent data from the NAHB / Wells Fargo Housing Market Index, which captures builder sentiment in the single-family housing market. It declined by two points to 35 in June, marking the 14th consecutive month of scores under 40. The last time the Index remained at such low levels for a sustained period was in the 2011-12 housing foreclosure crisis following the Great Recession.8

Promising Signs from Policymakers

In a housing market filled with headwinds, one potential tailwind is the Federal 21st Century ROAD to Housing Act, which aims to remove regulatory barriers to home building, modernize HUD programs, and enhance community banking operations. The Act passed the House and is currently under negotiation in the Senate. Should the Act pass, its impact is likely to be gradual and dependent on local implementation.9

At the state level, many bills with the same agenda as the 21st Century ROAD to Housing Act have been introduced to combat the housing shortage - Florida, Maryland, and Illinois have introduced bills that would promote housing development near public transportation while Virginia, Pennsylvania, and Michigan have introduced bills to limit parking minimums, making it easier to build housing in areas where less parking is needed.10

While the 21st Century ROAD to Housing Act and state-level zoning reforms would benefit the housing market in the long-term, such legislation takes time and these reforms will not immediately move the needle on housing starts.

Outlook for H2 2026

While a few industry analysts have made slight changes to their housing starts forecasts for 2026, overall mid-year projections remain in line with those from the beginning of the year.

| Industry Analyst | U.S. Housing Starts (2026P) | Implied YoY Growth |

|---|---|---|

| EIA11 | ~1.36M | 0% |

| Fannie Mae12 | ~1.35M | -0.5% |

| NAHB13 | ~1.34M | -1% |

| Deloitte14 | ~1.34M | -1% |

| J.P. Morgan15 | ~1.30M | -4% |

| Wells Fargo16 | ~1.30M | -4% |

| Overall Average | ~1.33M | -2% |

Earlier this year NAHB projected 1.38M housing starts but has since lowered its projection to 1.34M while EIA and Fannie Mae have increased their earlier projections of 1.32M and 1.29M, respectively. Although single-family starts have underperformed many analysts’ projections, multifamily starts have overperformed and helped keep overall projections in line. However, the recent drop off in multifamily starts in May is not captured in these projections and will likely impact future updates.

The outlook for the rest of 2026 is continued softness with starts hovering at a ~1.35M annualized rate rather than recovering toward the 1.40M+ range that seemed possible in Q1. Until mortgage rates move meaningfully lower or affordability improves markedly, U.S. housing starts will likely remain compressed. If the Iran war continues well into H2 2026, bringing further instability to oil markets and broader macro-economic uncertainty, starts will likely fail to meet current expectations.

Interested in learning more about Bantry Partners’ deep expertise and experience in the construction and building products industry? Contact us at info@bantrypartners.com

CITATIONS

[1] United States Housing Starts

[2] New Residential Construction Press Release

[3] May Housing Starts Fall as Multifamily Construction Slows Sharply | NAHB

[4] Builder Sentiment Posts Notable Decline on Economic Uncertainty | NAHB

[6] Mortgage Rates - Freddie Mac

[7] TD Economics - U.S. Housing Starts and Permits (May 2026)

[8] Builder Sentiment Remains Weak Amid Affordability Concerns | NAHB

[10] On zoning and housing, states continue to take charge - Smart Growth America

[11] Short-Term Energy Outlook

[12] Housing Forecast - May 2026

[14] US Economic Forecast Q1 2026 | Deloitte Insights