Despite Headwinds, Automotive Aftermarket Is Poised For Growth

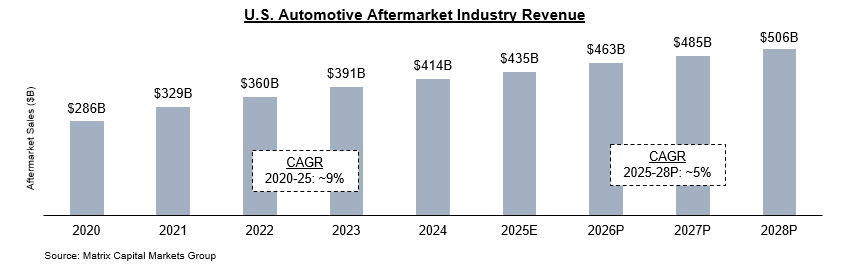

The automotive aftermarket in the U.S. is a massive and relatively “recession resistant” industry, valued at ~$435B in 2025. The increasing number of vehicles in operation and the increasing age of vehicles are positive growth drivers for the industry. Despite headwinds such as the proliferation of EVs, tariffs, and constrained labor supply, steady growth is still expected, and industry sales are projected to eclipse $500B by 2028.1

At Bantry Partners, we have deep expertise in the automotive aftermarket from advising PE investors on dozens of deals in the industry over the past 20+ years. Here are some of the key trends to watch:

Vehicle population continues to expand

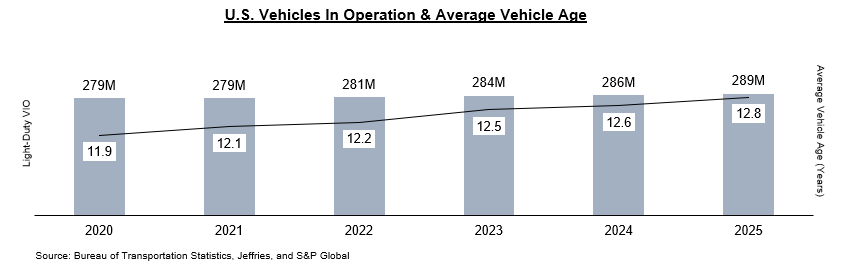

The number of light-duty vehicles in operation in the U.S. (the “car parc”) reached 289M in 2025, an increase of ~3M over 2024. The composition of the car parc has been gradually shifting towards trucks (pickups, SUVs, and vans) and away from passenger cars for the last 50 years. 2025 marked the first time since the early 1970s that the number of passenger cars in operation dipped below 100M.2,3

This transition bodes well for the aftermarket as light-duty trucks typically have higher lifetime maintenance costs than passenger cars. The average sedan incurs only ~$700 in maintenance per year compared to ~$910 for the average SUV and ~$1,030 for the average pickup truck.4

Number of vehicles in the sweet spot for the aftermarket continues to grow

Vehicles aged between 4 to 11 years are the sweet spot for aftermarket parts and repairs spending – they have aged out of OEM warranties but still have sufficient lifespan remaining to justify consumers investing in maintenance. The number of vehicles in this sweet spot has grown at a CAGR of ~5% so far this decade to reach ~119M in 2025. In 2025, the average age of light-duty vehicles was 12.8 years – an increase of ~4 months since 2023.2

This is a positive driver for the aftermarket as consumers are electing to spend money on maintaining current vehicles rather than buying new vehicles. Recent inflation in the pricing of new vehicles is also contributing to many consumers opting to keep (and maintain) their current vehicles for longer.

Electric vehicles (EVs) will continue to grow but do not pose an immediate threat to the aftermarket

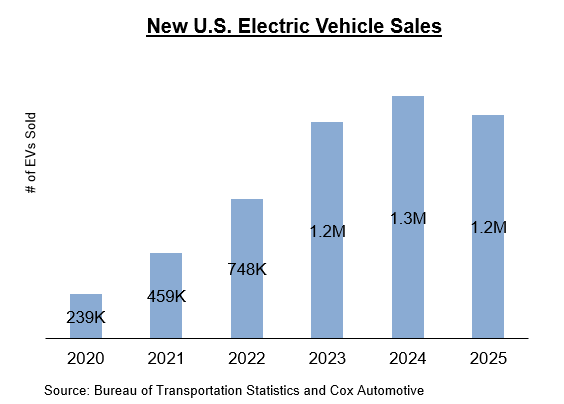

Adoption of electric vehicles is viewed as a negative for the automotive aftermarket because of their simpler maintenance needs and lower maintenance costs. While EVs have seen strong sales growth in recent years, the U.S. car parc will remain dominated by internal combustion engine (ICE) vehicles for the foreseeable future. EV sales in 2025 were down 2% from 2024, marking the first YoY decline since 2019.5

Some U.S. OEMs are now shifting their near-term focus away from EVs. Last year, Stellantis canceled plans for the EV Jeep Gladiator and EV Ram pickup truck. Most of its $13B investment in new U.S. manufacturing capacity will go towards four new ICE models.6 General Motors and Ford announced plans to unwind some of their EV investments and will be taking charges of $6B and $19.5B, respectively.7 In 2021, GM set a goal of producing only EVs by 2035 and although they “still believe in an all-EV future,” recent production decisions show that it is not a near future.8

Tariffs are a significant and fluid headwind for the automotive aftermarket

In May 2025 a 25% tariff went into place on imports of automobiles and 150 different parts categories including engines, transmissions, bumper components, tires, and windshields.9 Exceptions include parts that qualify under the USMCA, which are exempt from the tariff, parts from the United Kingdom (subject to a 10% tariff), and parts from the EU, Japan, and South Korea (subject to a 15% tariff).10 In late January, President Trump announced an increase in South Korea’s tariff from 15% to 25% (retroactive to November 1, 2025), but as of the time of posting, it has not yet taken effect.11

To navigate supply chain disruptions caused by tariffs, aftermarket service providers are seeking new domestic supply chains, while parts OEMs are looking to reshore or nearshore manufacturing. However, the volatility around tariffs continues to fuel uncertainty – parts OEMs worry about moving operations to currently exempt countries only to see those countries saddled with tariffs later. Representatives from the Motor & Equipment Manufacturers Association have also met with Federal agencies involved in tariff decisions to advocate on behalf of the aftermarket.12 Despite the tariff headwinds, the aftermarket industry still posted strong sales of ~$435B in 2025 and continued its historical resilience to disruptive economic forces.1

Supply of auto technicians will shrink over the next decade

As in many of the trades, the growing shortage of automotive technicians in the U.S. will lead to higher labor rates and prices for consumers and longer lead times and delays for service and repair work. PE investors looking to invest in auto repair businesses should take into account how the labor shortage could impact their investments in a myriad of ways, from margins to their ability to expand operations.

Currently, there are ~800K auto technicians in the U.S. Over the next decade, there are projected to be ~70K job openings for technicians each year as the industry grows and current techs move to different occupations or retire.13 Only ~40K of these jobs will be filled by new technicians graduating from technical colleges and training programs, which leaves a shortage of ~30K jobs unfilled each year. The National Automobile Dealers Association is working to provide scholarships to technical colleges and access to training programs to bring more new talent into the industry.14 Aftermarket service providers will need to support this initiative and recruit new talent to combat the expected shortages over the next decade. A strong talent acquisition and retention strategy for technicians should be a key element of any PE investor’s plans for investing in this industry.

Interested in learning more about Bantry Partners’ expertise in the automotive aftermarket? Contact us at info@bantrypartners.com

CITATIONS:

[1] Automotive Aftermarket Sector Update - Summer 2025 | Matrix Capital Markets Group

[2] Average Age of Vehicles in the US Hits 12.8 Years in 2025 | S&P Global

[3] Alternative Fuels Data Center: Maps and Data - Composition of New U.S. Light-Duty Vehicles by Vehicle Type

[4] 10 American Pickup Trucks That Have High Maintenance And Repair Costs

[5] Despite Q4 Collapse, 2025 EV Sales Decline Only 2% Versus 2024; Policy Shifts, New Product Set Stage for Next Chapter - Cox Automotive Inc.

[6] Stellantis to Invest $13 Billion to Grow in the United States | Stellantis

[7] GM to take $6 billion writedown on EV pullback | Reuters

[8] GM slow-rolls its all-EV aspirations - POLITICO

[9] Understanding the New Tariffs and their Potential Impact on Auto Repairers - Automotive Service Association - National

[10] Section 232 Automotive Tariffs: Issues for Congress | Congress.gov | Library of Congress

[11] White House Spokesperson Says 'No Timeline' on South Korea Tariff Hike

[12] Frustrations grow for aftermarket suppliers as trade policy repercussions mount - Aftermarket Matters

[13] Automotive Service Technicians and Mechanics : Occupational Outlook Handbook: : U.S. Bureau of Labor Statistics