Outlook for U.S. Housing Starts in 2026

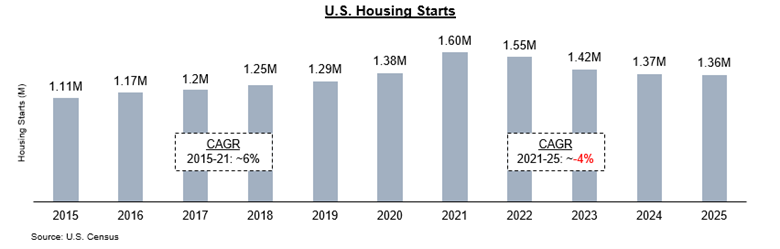

Home builders in the U.S. have faced significant headwinds in the years since the COVID pandemic, with 2025’s tally of ~1.36M housing starts marking the fourth consecutive year of decline – and well below the ~1.7M units some experts estimate are needed annually to keep pace with U.S. population and household formation growth.1

High home price-to-income ratios, elevated mortgage rates, and persistent building material and labor expenses have impacted both home builders and buyers alike. These conditions are expected to persist in the near-term and 2026 seems likely to be another year of minimal to negative growth in housing starts and ongoing buyer and builder frustration.

At Bantry Partners, we have deep expertise in the construction and building products industry from advising PE investors on dozens of deals in the sector over the past 20+ years. Here are some of the key trends to watch:

Continued Stagnation in Housing Starts Expected in 2026

Given the labor, material, and financing constraints squeezing home builders and buyers, most industry forecasters expect flat to negative growth in U.S. housing starts in 2026. The industry’s trade association - the National Association of Home Builders - expects single-family housing starts to increase by only ~1% in 2026 to 940K units while multi-family starts are expected to decline by ~5% to 392K units.2 Fannie Mae is more bearish on single-family starts, projecting a ~3% decline to 901K units in 2026.3 Other reputable forecasters share broadly similar expectations:

| Industry Analyst4 | U.S. Housing Starts (2026P) | Implied YoY Growth |

|---|---|---|

| NAHB2 | ~1.38M | 1% |

| Wells Fargo5 | ~1.38M | 1% |

| Deloitte6 | ~1.34M | -1% |

| EIA7 | ~1.32M | -3% |

| J.P. Morgan8 | ~1.30M | -4% |

| Fannie Mae3 | ~1.29M | -5% |

| Overall Average Outlook | ~1.34M | -2% |

Synthesizing across these industry analysts, a reasonable projection for 2026 U.S. housing starts ranges between ~1.32M to 1.35M units - a ~2% decline from 2025 and a ~3% decline from the recent peak in 2021.

Home Builders Face Significant Challenges

Labor shortages and high building material costs are key factors dragging on home construction. There were ~300K job openings in the construction industry in December 2025, an increase of 50% over the same period in 2024. The Trump Administration’s immigration policies will continue to have a negative impact on labor supply for construction projects. The National Association of Home Builders (NAHB) estimates that ~740K new workers will be needed annually to keep pace with growing demand and replace workers aging out of the industry.

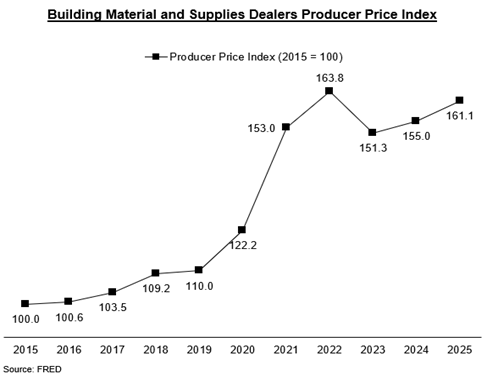

Building material costs are also impacting construction levels as overall inflation has remained above 3% since June 2025.9 As seen in the Producer Price Index chart below, prices for building materials are slightly down from the peak in 2022, but still ~50% above pre-COVID levels. Prices are expected to remain elevated throughout the year, and while it is not a full year average and should not be viewed as a direct comparison, the January 2026 Index stands at 182.5, ~22% higher than 2025.

While demand for housing remains strong at a structural level, it is being suppressed by financing conditions rather than a lack of need. NAHB estimates the total U.S. housing shortage at ~1.2M units currently. The need for housing in the U.S. remains robust, but new starts will see little growth unless there is significant regulatory action at a Federal level to lower construction costs and mortgage rates.2

Mortgage Rates Remain High

As of March 12th, the U.S. average 30-year fixed-rate mortgage (FRM) is 6.11%, down from 6.65% in March 2025. While an improvement, it is not the dramatic rate reduction needed to meaningfully improve housing affordability and unlock large-scale housing demand, especially for first-time buyers.10

The consensus across major forecasters is that mortgage rates have already bottomed out, and meaningful rate reductions are unlikely to be seen until 2027 at the earliest (see table below). The Chief Economist for NAHB says, “A sustained sub-6% mortgage rate will likely wait until 2027.”2

| Industry Source11 | 2026 Average 30-year FRM |

|---|---|

| NAHB | 5.99% |

| Fannie Mae | 6% |

| National Association of Realtors | 6% |

| Wells Fargo | 6.14% |

| Mortgage Bankers Association12 | 6% - 6.5% |

If rates were to fall more sharply than anticipated due to a Federal Reserve policy shift, a cooling labor market, or declining inflation, the upside for U.S. housing starts could be significant. But at the time of writing, most forecasters are not expecting any significant changes in 2026, although pending leadership changes at the Fed in mid-2026 could alter this picture.

New Home Prices Are Stabilizing

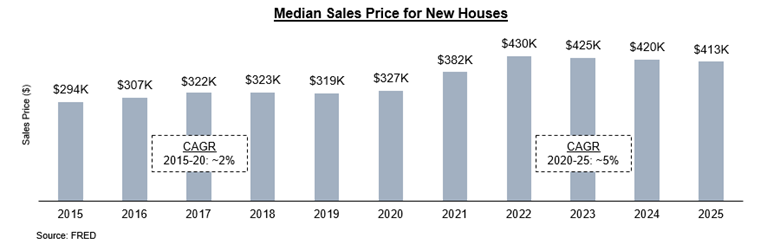

After three consecutive years of growth, the median sales price of new homes in the U.S. reached a peak of ~$430K in 2022. The past two years have resulted in a modest decline, with the median price falling to ~$413K in 2025.13 Many builders have recently deployed strategies such as mortgage rate buydowns and price reductions to meet buyers where affordability allows them to. This behavior is expected to continue to some extent, and new home prices are expected to remain relatively stable in 2026.11

Final Thoughts

For policymakers, home builders, and buyers alike, the message from forecasters is consistent: meaningful improvement in housing affordability and new construction will require either a more substantial decline in mortgage rates than currently projected, significant regulatory reforms to lower construction costs, or both.

Interested in learning more about Bantry Partners’ deep expertise and experience in the construction and building products industry? Contact us at info@bantrypartners.com

CITATIONS

[1] New Residential Construction Press Release

[2] 2026 Housing Outlook: Ongoing Challenges, Cautious Optimism and Incremental Gains | NAHB

[3] Housing Forecast - February 2026

[4] 2026 Mortgage Rate Forecast: When Will Rates Go Down?

[5] Wells Fargo - U.S. Housing Forecast

[6] US Economic Forecast Q4 2025 | Deloitte Insights

[8] Macro & Markets Midyear Outlook

[9] 2026 Housing Outlook: Ongoing Challenges, Cautious Optimism and Incremental Gains | NAHB

[10] Mortgage Rates - Freddie Mac

[11] 2026 Mortgage Rate Forecast: When Will Rates Go Down?

[12] MBA Solidifies 2026 Forecast – NMP

[13] Median Sales Price for New Houses Sold in the United States (MSPNHSUS) | FRED | St. Louis Fed