AI, SaaS, And The Hype Cycle: Bubble Fears Or Structural Shift?

Bantry Partners has vast experience supporting middle-market private equity funds and their portfolio companies in the software and technology space. In recent weeks, many of our clients have faced what some have deemed a "software reckoning," with doomsayers reporting that AI-driven displacement may have driven drastic drops in the valuations of many SaaS investments. In many cases, software valuations have reset sharply. The private equity market continues to be highly vulnerable, with PitchBook reporting that software accounted for 18% of U.S. PE deal value in 2025 alone¹.

"There is a lot of fear in the market. So many funds are heavily invested in software, particularly SaaS solutions. If AI truly is going to disrupt those investments, the damage to the market will be unlike anything that we've seen in the (PE) middle market." Managing Director, Middle Market Private Equity Firm

Enterprise software has long been built on predictability. Recurring revenue models, embedded workflows, and integration complexity created businesses that investors viewed as both scalable and defensible. That foundation is now being reassessed. Public software stocks have been volatile, growth multiples have declined, and investors are asking harder questions about durability as AI reshapes the competitive environment.

The debate isn’t whether AI is real. It clearly is. The real question is whether AI meaningfully disrupts the SaaS model, or reshapes it in ways that strengthen the strongest platforms while exposing the weakest. History suggests those two outcomes can happen at the same time.

Has there been a structural shift in the market? Or are the bubble fears overhyped?

Are We at Peak AI Hype?

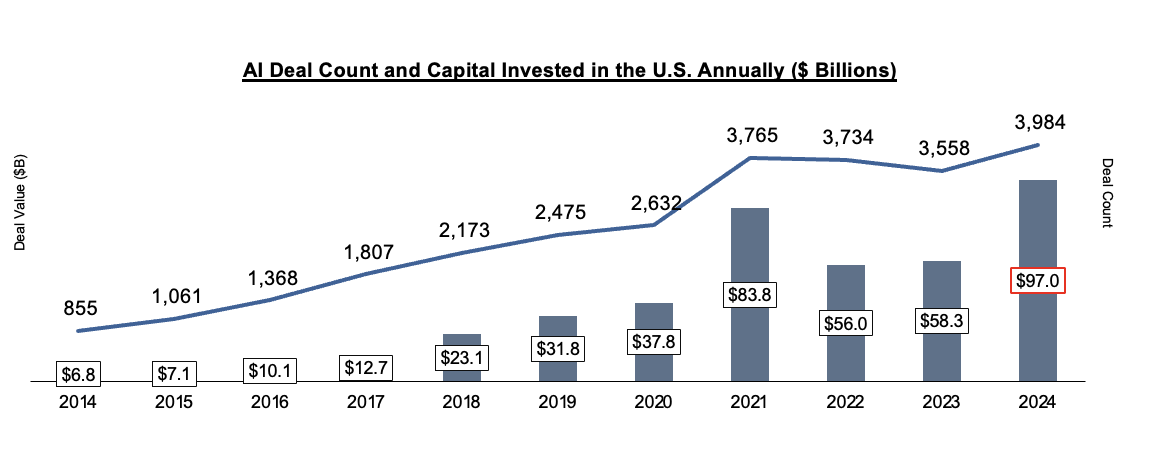

Every major technology cycle blends genuine innovation with heavy capital concentration. U.S. venture capital investment into AI-related companies surged between 2022 and 2024, representing a record share of total venture funding according to NVCA data². In several recent quarters, AI accounted for more than one-third of all U.S. venture dollars deployed. That level of concentration naturally raises eyebrows.

Source: 2025 Pitchbook

At the same time, enterprise adoption is not speculative. Companies are not just experimenting — they are implementing.

"AI isn't coming. It's here. Usage among companies is steadily rising and is poised to take off as more applications become evident. I know our portfolio companies are diligently looking for ways to utilize AI." Principal, Middle Market Private Equity Firm

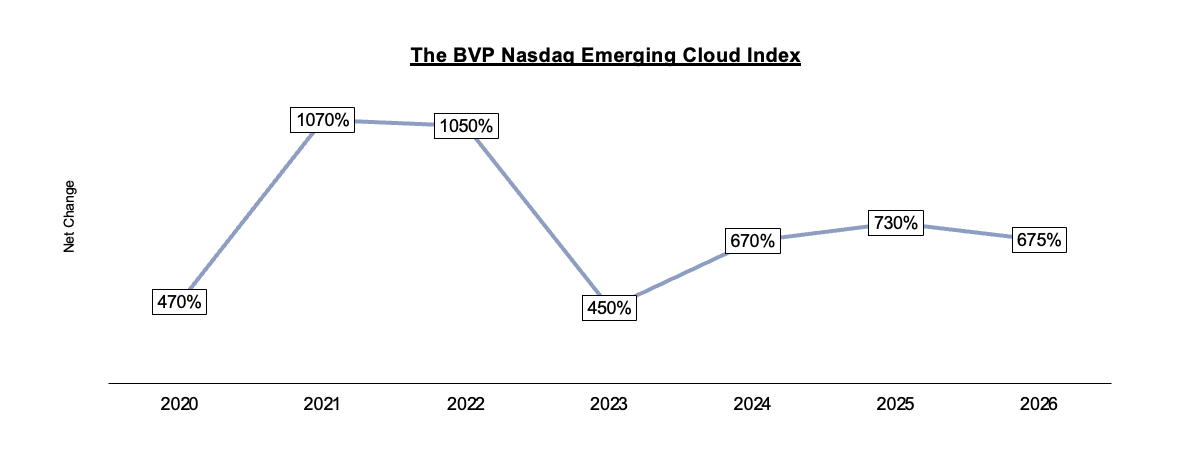

Valuations, however, tell a more tempered story. The BVP Nasdaq Emerging Cloud Index remains well below its 2021 peak³. Software has already been repriced in a higher-rate environment.

Source: NASDAQ

The Federal Reserve has repeatedly highlighted asset valuation sensitivity in high-growth sectors during tightening cycles⁴, and software multiples have reflected that sensitivity. This does not resemble unchecked mania. It looks more like a structural transition occurring alongside a cost-of-capital reset. Hype may exist at the edges, but real adoption and real repricing are happening simultaneously. This is also evident in the PE middle market, where valuations and multiples for software companies are under pressure.

"After years of sky-high multiples, there has been a correction. Has every fund realized this yet? No. But the recent worries regarding AI have changed that. We're not seeing many software deals that are coming to market, and those that are, are not at multiples that we saw even 18 months ago." Managing Director, Middle Market Investment Bank

The Bear Case: Where AI Could Pressure SaaS Economics

There is a credible downside scenario for parts of the SaaS ecosystem, though it is likely to unfold gradually rather than abruptly. The pressure would show up in slower growth, shorter competitive cycles, and potential multiple compression. One area of concern is moat compression. AI-assisted development tools are shortening build timelines. Features that once required months of engineering effort can now be developed far more quickly. If a SaaS company’s differentiation is primarily feature-based rather than rooted in deep workflow integration, the barrier to replication narrows. Speed alone is no longer a durable moat.

Another frequently cited risk is the internal build argument. AI lowers the cost of writing software, and the Bureau of Labor Statistics continues to report strong growth in software developer employment and productivity⁵. Some interpret this as a potential return to in-house builds, particularly for non-core systems. But enterprises moved away from internal software projects for structural reasons: ongoing maintenance costs, security vulnerabilities, integration challenges, and the distraction from core business priorities. AI may reduce upfront development time, but it does not eliminate long-term support, compliance, or upgrade burdens. For mission-critical systems, those considerations remain significant.

There is also the rise of AI-native entrants. New companies launching today can design their stacks around AI from inception. They are not constrained by legacy architectures. While this does not automatically displace incumbents, it may affect long-term share capture in emerging categories.

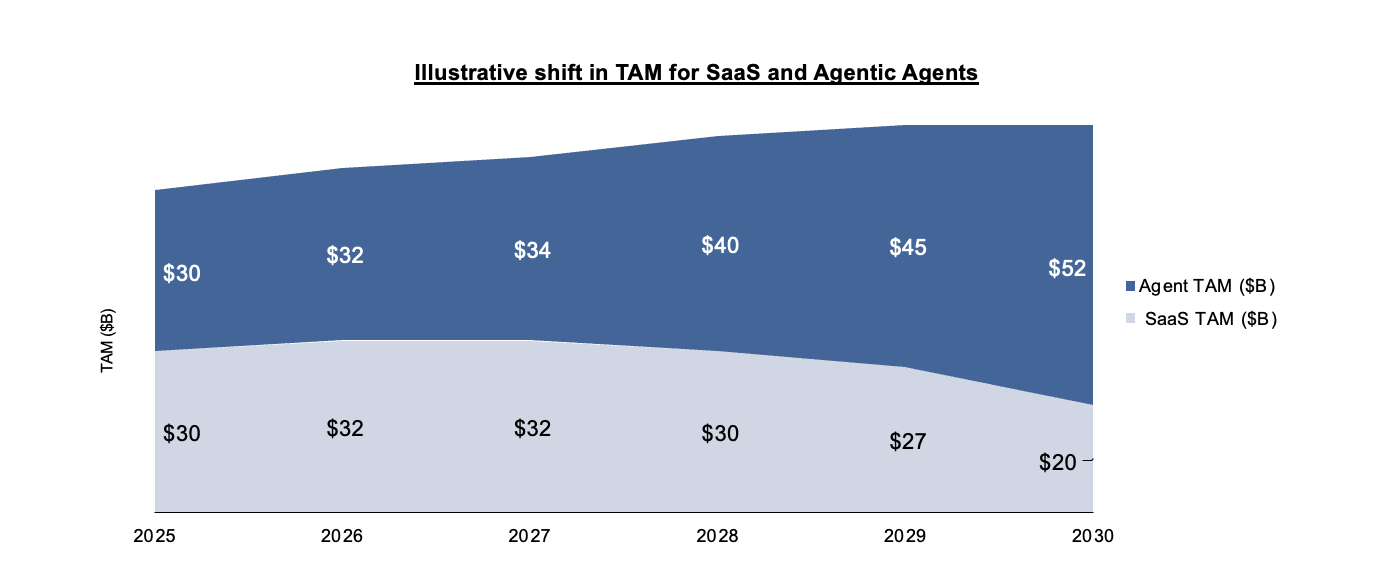

However, the bear case isn’t that software demand disappears. It’s that the economics migrate. Projections from Gartner and Goldman Sachs suggest that traditional SaaS markets could plateau later this decade, while AI agent platforms could grow rapidly. If automation layers begin capturing workflow value that once resided in subscription applications, revenue durability for some vendors could come under pressure¹⁰.

Source: Gartner, Goldman Sachs Research

Taken together, the bear case centers less on SaaS disappearing and more on durability assumptions being tested. If investors are underwriting extended competitive cycles, they must consider whether those cycles are compressing in an AI-accelerated environment.

Why SaaS Incumbents May Be More Resilient Than Headlines Suggest

Disruption narratives often underestimate the structural stickiness of enterprise software. Core systems such as ERP, CRM, HCM, and financial platforms are deeply embedded into daily operations. Government Accountability Office modernization reviews consistently show that large-scale system migrations take years and require significant capital and organizational effort⁶. These are not casual switching decisions. Switching costs extend beyond licensing fees. They include workflow redesign, data migration, integration across multiple systems, regulatory validation, and workforce retraining. AI does not remove those frictions.

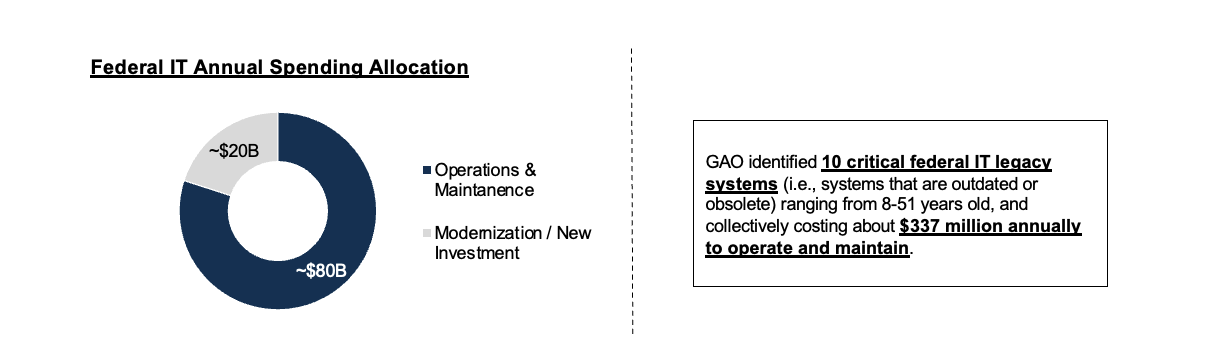

The federal government spends more than $100 billion annually on IT—with roughly 80% allocated to maintaining existing systems—and even among the 10 most critical legacy platforms, some are more than 50 years old and collectively cost over $337 million per year to operate, underscoring how deeply embedded, expensive, and difficult-to-replace core systems can be.

Source: U.S. GAO

Governance considerations further reinforce this dynamic. The National Institute of Standards and Technology continues expanding its AI Risk Management Framework⁷, signaling that enterprises—particularly in regulated industries—must approach AI implementation within structured oversight environments. Replacing a mission-critical SaaS platform with a lightly governed internal AI build is unlikely to become common practice overnight.

It is also important to note that incumbents are investing aggressively. Salesforce has announced plans to invest approximately $15 billion over five years to expand AI infrastructure and enterprise capabilities⁸. Major SaaS vendors are embedding AI directly into their existing platforms, often enhancing automation, analytics, and productivity features. In many cases, AI may reinforce incumbent solutions rather than undermine them. For mission-critical enterprise platforms, AI appears more likely to act as an enhancement layer than a replacement mechanism.

The Valuation Context: Why This Matters More in Today’s PE Environment

This conversation is unfolding within a private equity market defined by tighter liquidity and longer hold periods. Bain & Company’s Global Private Equity Report highlights elevated levels of unsold portfolio companies relative to prior cycles⁹. Exit timelines have stretched, and financing costs remain higher than they were during the zero-rate era.

Higher discount rates reduce the present value of long-duration growth. When holding periods extend, underwriting errors compound. If AI shortens competitive cycles or alters margin structures, those shifts directly influence exit multiples and IRR outcomes. In a more forgiving capital environment, growth optimism can mask durability risk. In today’s environment, it cannot. The AI–SaaS debate is therefore not just a technology discussion; it is directly tied to capital discipline.

What Investors Should Focus On

Rather than framing the issue as hype versus collapse, investors should focus on fundamentals. How mission-critical is the platform? What workflows does it truly control, and how deeply is it integrated across adjacent enterprise systems? What does churn look like across multiple economic cycles? Does the vendor demonstrate sustained pricing power?

"As we look at the software market, there is clearly a fundamental shift going on. But there are still plenty of opportunities as multiples become more realistic. Mission-critical software won't be replaced. Relationships and the service that many customers are used to also won't be replaced." Sr. Partner, Middle Market Private Equity Firm

Investors should also examine whether defensibility stems from proprietary data, regulatory positioning, or ecosystem dependencies rather than surface-level features. AI integration should be assessed pragmatically: is it improving margin structure and customer retention, or is it primarily cosmetic?

Finally, it is worth evaluating whether AI-native competitors are materially impacting win rates or whether installed bases remain stable. Dispersion across SaaS categories is likely to increase. Deeply embedded workflow platforms may strengthen, while feature-driven tools with limited defensibility could experience pressure.

AI cycles tend to feel binary as they unfold, but outcomes rarely are. AI is compressing development timelines and reshaping cost structures, yet switching costs, governance frameworks, and enterprise inertia remain powerful forces. SaaS is unlikely to disappear; it is far more likely to evolve. In a higher-rate, liquidity-constrained environment, distinguishing between durable platforms and fragile growth stories matters more than it has in years.

"There will be winners and losers, but are all SaaS investments now worthless? We don't see it that way. Don't believe the death tolls being rung. This will be difficult for some SaaS companies, but we don't think it's as bad as being advertised." Managing Director, Middle Market Private Equity Firm

Interested in learning more about Bantry Partners’ expertise in the SaaS market? Contact us at info@bantrypartners.com

CITATIONS:

[1] PE Exposure to Software Reckoning

[2] U.S. Venture Monitor Reports (2023–2025) | National Venture Capital Association (NVCA)

[3] BVP Nasdaq Emerging Cloud Index | Bessemer Venture Partners

[4] Financial Stability Report (2022–2025) | Federal Reserve

[5] Occupational Outlook Handbook: Software Developers | U.S. Bureau of Labor Statistics

[6] Federal IT Modernization and Oversight Reports | U.S. Government Accountability Office (GAO)

[7] AI Risk Management Framework | National Institute of Standards and Technology (NIST)

[8] Salesforce Investor Relations & Financial Disclosures | Salesforce

[9] Global Private Equity Report 2026 | Bain & Company

[10] AI Agents To Boost Productivity | Goldman Sachs, Gartner